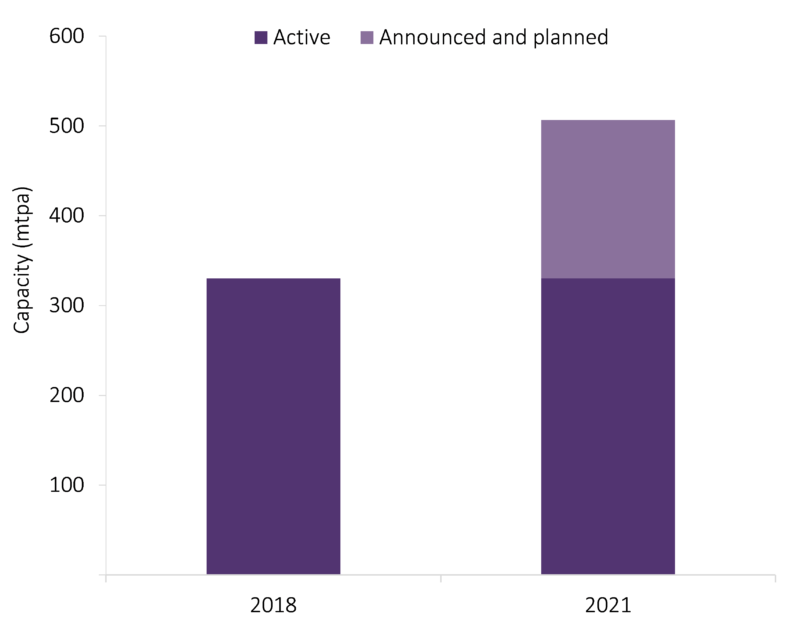

GlobalData’s latest analysis of the global liquefied natural gas (LNG) liquefaction capacity shows that Qatar has the highest LNG liquefaction capacity globally with 77.5 million tonnes per annum (mtpa) in 2018. Australia and Indonesia follow with 75.3mtpa and 32.1mtpa respectively.

Presently, Qatar accounts for 20.3% of the total global LNG liquefaction capacity. The country has eight active LNG liquefaction terminals. Presently there are no planned and announced projects that would start operations between 2018 and 2021.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Australia has a 19.7% share of the global LNG liquefaction capacity in 2018. The country has nine active LNG liquefaction terminals. The country will add capacity of 16mtpa from three planned and announced terminals during 2018 – 2021.

Indonesia contributes about 8.4% of the global LNG liquefaction capacity in 2018. Indonesia is expected to add a capacity of 2mtpa from a planned terminal during the period 2018 – 2021.

Global LNG Liquefaction Capacity

Source: GlobalData Midstream Analytics

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataThe fourth major contributor to the global LNG liquefaction capacity is Malaysia with 30.4mtpa, which is 8% of the global LNG liquefaction capacity in 2018. It has five active terminals. The country is expected to add a capacity of 1.5mtpa from a planned terminal during 2018 – 2021.

Algeria is the fifth largest contributor to the global LNG liquefaction capacity with 28.8mtpa, which accounts for 7.5% of the global total. Presently there are no planned and announced projects that would start operations during 2018 – 2021.

Nigeria contributes about 22mtpa to the global LNG liquefaction capacity in 2018, which is around 5.8% of the global LNG liquefaction capacity. Presently there are no planned and announced projects that would start operations during 2018 – 2021.

Russia contributes about 21mtpa, which is approximately 5.5% of the global LNG liquefaction capacity. Russia is expected to add a capacity of 3.1mtpa from four planned and announced terminals during 2018 – 2021.

The US, Trinidad and Tobago and Oman collectively contribute about 43.2mtpa, which is 11.3% of the global LNG liquefaction capacity. A total of 17 planned and announced terminals in the US are expected to add a capacity of 153.8mtpa between 2018 and 2021.