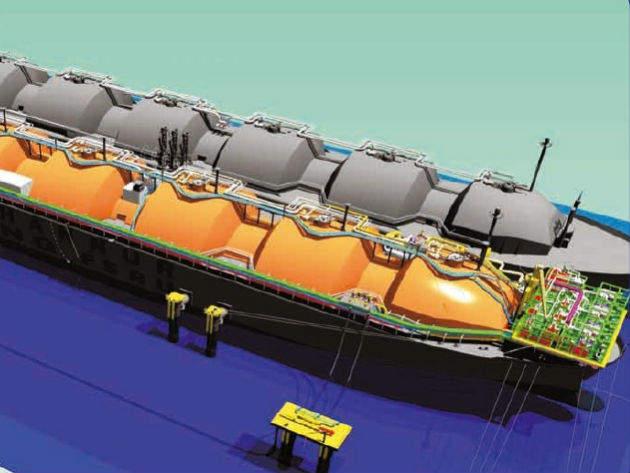

At this year’s SMi FLNG 2017 event, talk repeatedly returned to the growth and benefits of floating storage regasification units (FSRU). Compared to their onshore counterparts they require little construction or investment, and can therefore provide access to LNG much faster.

This has led to an increase in their usage throughout the world. In 2008 a mere 1% of regasification units were FSRUs, whilst in 2016 they made up 10%. This proportion looks set to continue to increase to 15% of the market by 2020, as Tony Tarrant, manager for midstream and LNG at Amec Foster’s Business Solutions Group, explored in his talk titled ‘Offshore versus land-based regasification terminals’.

Go deeper with GlobalData

Whilst on land units still dominate the industry, FSRUs provide some clear benefits, in particular for developing economies. But in the long term, are FSRUs the best gas strategy?

Which countries are embracing FSRUs?

FSRUs are predominantly popular in emerging economies as opposed to developed gas markets such as the US and Europe. “The majority of the FSRUs at the moment are located in Latin America, the Middle East and Asia regions where they were predominantly present compared to onshore LNG terminals,” says Sergio Gonzalez, Business Solutions Group midstream and LNG manager for Spain.

Last year there were 78 FSRUs online, with more under construction. Almost all were in countries with little previous LNG capacity – “likely emerging countries like Bangladesh, Vietnam, Pakistan, Philippines, Ghana and South Africa,” according to Gonzalez. These are predominantly countries which are experiencing industrial revolutions and modernisation. As workforces and day-to-day life increasingly require electrical power, governments are looking for fast ways of delivering reliable energy, and hitting on gas.

There are several reasons for the popularity of offshore regasification in emerging economies. “[FSRUs are] easier to finance due to less investment needs,” explains Business Solutions Group midstream and LNG manager for America Augusto Bulte. “[An] FSRU is delivered under a leasing contract that includes the facility and its operation and maintenance. CAPEX investment in these projects is limited to the mooring facilities and onshore receiving facilities [for which] which investment might be $100m.”

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataIn developing countries this initial reduction in investment is particularly important, as many would not be capable of investing the much higher amount of $400m necessary for an onshore terminal with the same capacity. This can provide a much easier entry into the LNG market, helping to develop economies by providing power to industry.

Speed is also a big factor

The limited CAPEX investment necessary is not the only benefit of offshore regasification; several other factors also feed into the popularity of FSRUs in less developed gas markets – most notably the speed with which they can come online.

The design, licensing and construction process are all shorter, so that an average floating unit will take a year less to start operations than a comparable onshore unit. Construction is only required for a jetty, subsea pipeline, and minimal onshore building. This means that “the schedule required for an offshore solution might be around 14-18 months, versus 24 months [for] a typical onshore solution with floating storage units or 38 months for a typical onshore with a full containment LNG tank,” explains Bulte.

This speed is essential for many countries for a variety of reasons, often due to fast increasing demand that goes alongside industrialisation and development. [Some] countries look for a temporary solution, either because they have indigenous gas that eventually will be exploited, or because their gas demand is seasonal. In such cases the onshore option is not the better,” adds Bulte.

Speed also allows countries to take advantage of the current low gas prices, which both benefit the consumers and encourages investment. In 2015, natural gas prices hit their lowest point since 1999, in part because of the glut created by fracking in the US. This low price can be exploited using FSRUs, as they are likely to come online quickly enough to make the most of low prices. “The level of development of the local economies and the important decrease in the LNG prices due the high number of recent actors starting to participate in LNG supplies at worldwide scale may stimulate the investors,” says Gonzalez.

What are the drawbacks?

There are downsides to choosing an offshore route for importing LNG, one of the most challenging being the lifespan of FSRUs. “Usually the leasing arrangements of FSRUs are for ten to twelve years,” Bulte says. “Longer agreements are not offered since they are not competitive versus an onshore solution.” Therefore a country’s long-term strategy for LNG imports is a crucial factor when considering offshore or onshore.

Bulte adds: “Technically an FSRU can be operative 20 years after building it, possibly more with the appropriate overhauling. Onshore terminals are designed to last 25 years at least; however there are onshore LNG terminals with almost 40 years in operation – for example Barcelona’s original regasification train.” The operating lifespan of an FSRU is further affected by the wear and tear caused by the offshore environment, as a floating regasification unit will suffer greater weather exposure.

Offshore units provide little possibility of expansion, as their capacity is limited by the size of the vessel. A standard FSRU has a maximum regasification capacity of 600-800 million standard cubic feet per day (MSCFD), and a new FSRU can store between 140,000m³ and 180,000m³ of gas. In an offshore facility a single train is capable of vaporizing just 40 MMSCFD or less; however, most facility will have multiple (usually five or more) trains increasing their total capacity to 1500-2000 MSCFD. Unlike FSRUs, however, onshore sites have no limit to storage capacity as long as there are no plot restrictions.

Whilst offshore regasification units boast smaller CAPEX, its higher OPEX may act as a drawback. An onshore unit will cost around $ 130,000 per day (4 MTPA), whilst an FSRU is likely to be around around $ 280,000 per day (4 MTPA). The increased OPEX costs are largely due to the high leasing rate of an FSRU.

Higher OPEX rates rely on a number of factors, and for many project this will not dissuade investors. The location of FSRUs in emerging economies, may do, as security instability issues may also affect the investment decisions significantly, says Bulte. The security of investments may become a concern when the units are moored in more dangerous regions, with geopolitical instability affecting the ability of projects to get off the ground.

There is a wide range in both limitations and benefits to FSRUs, but the choice hinges on the long-term energy goals of the investing country. “Long-term players in the industry do not really choose FSRU solutions for their projects,” explains Bulte. “Known concerns are the lower availability and reliability of the FSRUS versus onshore, as well as the high costs of the leasing rates. However, for those new players, which are mostly interested in fast-track solutions, with minimum initial CAPEX, the mentioned limitations are not a big issue.”