The global hydrogen economy is evolving, entering a new inflection point in 2026 amid shifting market realities, changing policy landscapes, and critical execution challenges.

As of February 2026, active low-carbon hydrogen capacity stood at around 2.2 million tonnes per annum (mtpa), with over 460 projects in operation, compared to 104 in 2020. Yet, despite this impressive increase in the number of active projects, capacity additions remain far below the levels needed to meet the near-term targets set by the IEA Net Zero Emissions (NZE) scenario.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

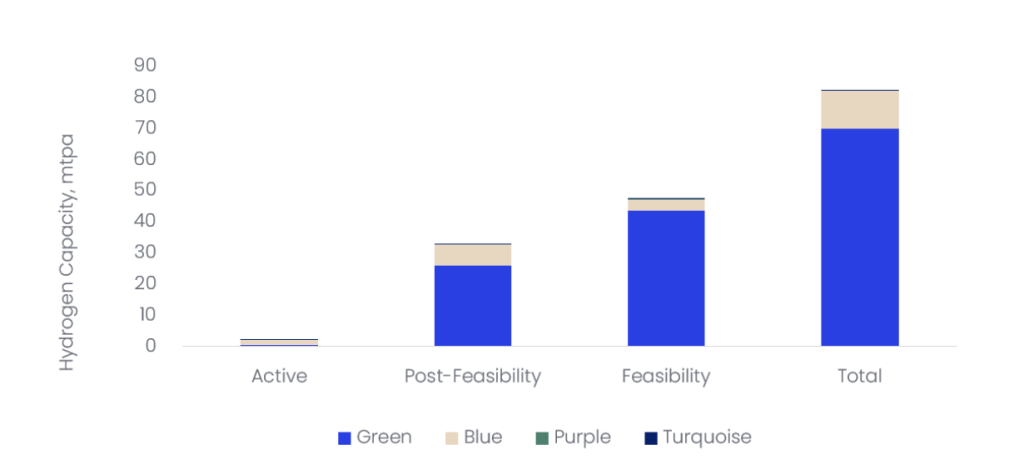

Looking ahead to 2030, global hydrogen production capacity is anticipated to reach 82.3mtpa, considering active under-development projects. As of now, only about 2% of this capacity stems from plants that are currently operational. Another 26% of the capacity is from projects that are in an advanced stage of development and hold a higher likelihood of completion before 2030. The remaining plants are still in early development, with around 57% of the capacity currently sitting in the feasibility stage.

The hydrogen development landscape is characterised by a notable scarcity of large-scale projects. Only ten of the 2,335 upcoming projects worldwide have capacities exceeding 1mtpa and a handful of others surpass the 0.5mtpa mark. Among these ten high-capacity projects, nine are for green hydrogen, and one is intended to produce blue hydrogen.

Among oil and gas majors, BP leads in terms of green hydrogen, with approximately 3mtpa of active and upcoming capacity anchored by flagship projects in Mauritania, Australia, and across Europe. TotalEnergies has also deepened its focus on green hydrogen projects, alongside industrial gas leaders such as Air Liquide and Air Products. Meanwhile, Shell and Equinor could be leaders in blue hydrogen capacity by 2030.

Global low-carbon hydrogen capacity, 2030

Green hydrogen leads the total low-carbon hydrogen announced capacity

In the long term, global low-carbon hydrogen capacity is expected to expand once demand picks up, backed by increased private investment and supportive policy frameworks, as it is a critical energy source for achieving corporate net-zero commitments. Major producing regions—including the US, Europe, China, and the Middle East—are anticipated to deliver the bulk of this future capacity growth. Nevertheless, achieving these ambitions will require overcoming persistent financial, regulatory, and infrastructure barriers in the near term to ensure that project announcements translate into operational capacity by the end of the decade.

Further discussion on initiatives from oil and gas companies in line with low-carbon hydrogen adoption and related trends can be found in GlobalData’s latest theme report, ‘Hydrogen in Oil and Gas’.