The biofuels sector is experiencing significant growth and transformation, driven by the urgent need to decarbonise the energy landscape and diversify fuel sources. Renewable fuels, a type of biofuel, are derived from naturally replenishing, nonedible biomass that provide a sustainable alternative to petroleum fuels and also to biofuels produced from edible crops such as corn and sugarcane.

Government policies and international regulations are driving biofuel adoption across multiple sectors, but policy support remains uneven globally. Many countries have implemented mandates for blending biofuels with gasoline, diesel, and jet fuel to curb emissions. Even in shipping, the International Maritime Organization is promoting biofuel use. However, policy approaches vary widely around the world. While the EU enforces strict mandates such as the ReFuelEU Aviation initiative requiring a minimum of 2% sustainable aviation fuel blending by 2025, some of the other regions lack such clear policies, leading to disparities in biofuel adoption and investment. The commitment of a nation to achieving interim net-zero objectives, availability of biomass, and affordability of petroleum fuels are critical factors influencing policy support for biofuels.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Despite their clean energy profile, biofuels face significant challenges, primarily related to production costs and competition with petroleum fuels. Processing advanced biomass sources such as agricultural and forestry waste remains expensive, limiting large-scale commercial viability. However, refiners such as Neste, Valero, and Marathon Petroleum are making strategic investments to scale biofuel production from these sources and thus lower costs. Feedstock diversification and technological innovations in refining are also critical to improving biofuel affordability and availability. Hence, although biofuels contribute towards energy security while reducing emissions, their adoption remains relatively nascent and restricted to certain markets globally. As a result, companies are cautious while pledging investments for new facilities, and even halting project development due to market uncertainties, as was seen in the case of Shell’s upcoming facility in Rotterdam.

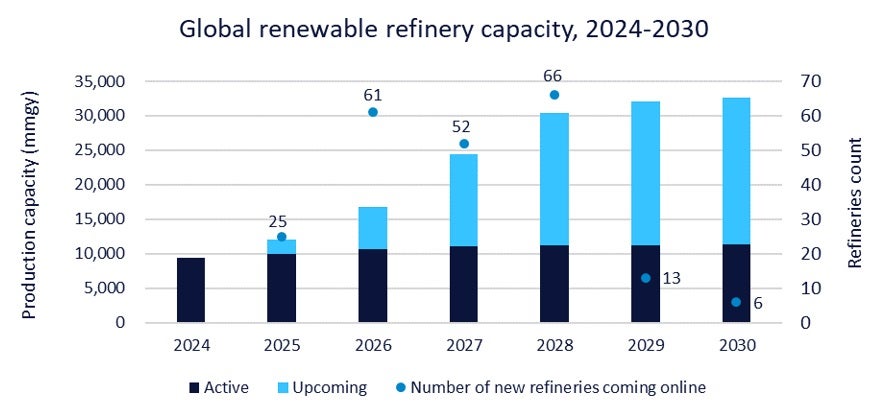

Global renewable refinery capacity is experiencing significant growth, with 15 new facilities under construction in 2025 and two, Rayong in Thailand and Bratislava in Slovakia, already operational this year. By 2030, an additional 218 facilities are expected to come online, expanding the global capacity from 9,340 million gallons a year in 2024 to a projected 32,618 million gallons a year. The US currently accounts for a 51% share in global renewable fuel production, driven by policy support and incentives such as the Inflation Reduction Act (IRA) of 2022 and California’s Low Carbon Fuel Standard. However, the recent political shifts in the country – including President Trump’s efforts to repeal certain provisions of the IRA, have introduced uncertainty in the policy environment.

Further discussion on the biofuels theme and its impact on the oil and gas industry, along with an overview of the competitive positions held by oil and gas companies, can be found in leading data and analytics company GlobalData’s new theme report, Biofuels.