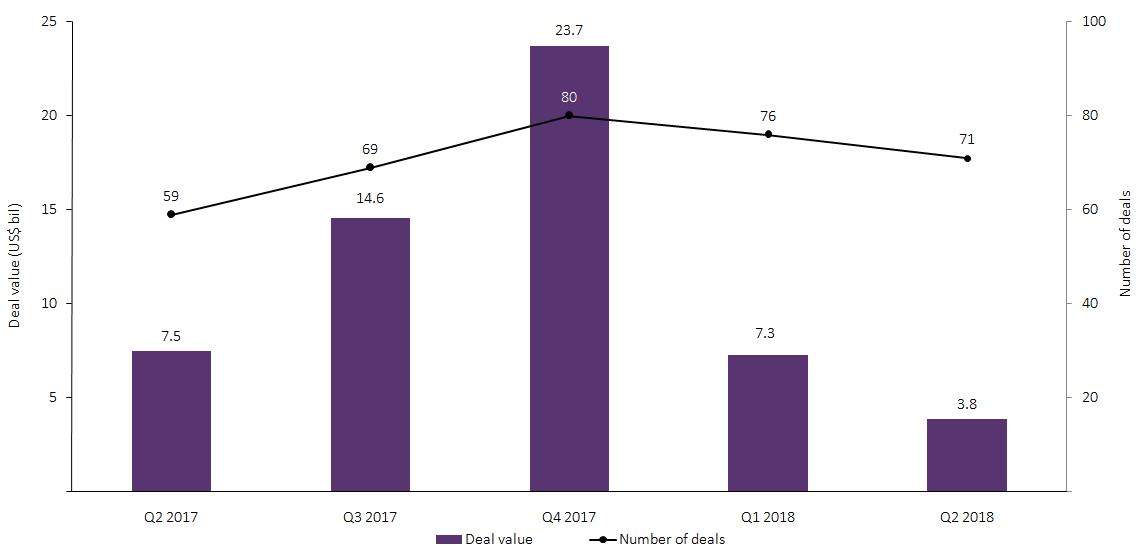

GlobalData’s latest report, Quarterly Equipment and Services Deals Review – Q2 2018, shows that a combined value of $3.8bn in mergers and acquisitions (M&A) were announced in the equipment and services sector in Q2 2018. This was a 48% decrease from the $7.3bn in M&A deals announced in the previous quarter. A year-on-year comparison shows a decrease of 49% in deal value in Q2 2018, when compared toQ2 2017’s value of $7.5bn. During the quarter, there were six M&A deals with values greater than $100m, together accounting for $3.2bn.

Weir Group’s acquisition of ESCO, for an estimated enterprise value of $1.3bn, was the top deal registered in Q2 2018. Under the terms of the transaction, 41% of the consideration will comprise new Weir shares and the remaining 59% of the consideration will be settled in cash. ESCO is an independent designer, manufacturer, and provider of wear and replacement products and services used in mining, oil and gas, construction, and industrial applications. The acquired ESCO will operate as a new division of the Weir, and will be reported as a separate segment alongside minerals and oil & gas. Goldman Sachs International and UBS Limited acted as financial advisors and joint corporate brokers to Weir Group in the transaction.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Equipment and services M&A deal value and count, Q2 2018

Source: Deals Analytics, GlobalData Oil and Gas © GlobalData

On the volume front, the number of M&A deals increased by 7% from 76 in Q1 2018 to 71 in Q2 2018, of which 23 were cross border transactions and the remaining 48 were domestic transactions. Americas was the destination of choice for cross-border M&A activity in Q2 2018, recording 10 cross-border transactions in the quarter.

Regionally, the Americas led the global M&A market in terms of volume and deal value, with 46 deals worth a combined value of $2.9bn, representing 65% of the global deals and 76% of the total value in Q2 2018. EMEA accounted for 24% share in Q2 2018, comprising 17 acquisitions, of which nine were cross-border and the remaining eight were domestic acquisitions, while Asia-Pacific region accounted for nine global deals, or 13% in Q2 2018, of which four were cross-border acquisitions and the remaining five were domestic acquisitions.