Carbon capture, utilisation and storage (CCUS) has emerged as a critical enabler of the global energy transition, particularly in the decarbonisation of hard-to-abate sectors such as cement, steel, refining and thermal power generation. Unlike other sustainability measures that are driven by consumer behaviour, such as the adoption of electric vehicles or energy efficiency upgrades, the uptake of CCUS is largely shaped by regulatory frameworks and economic incentives. This is because its primary applications are in upstream operations and heavy industry, which are far removed from end-users. As a result, strong policy tools —such as the EU Emissions Trading System, Canada’s carbon pricing mechanism and the US 45Q tax credit — have played a pivotal role in making CCUS economically viable. These policies are helping to unlock large-scale deployment opportunities, particularly in sectors that face significant barriers to emissions reduction.

The energy sector, especially oil and gas companies, has taken the lead in advancing CCUS technologies. As of 2024, more than 80% of operational and planned carbon capture facilities are associated with energy assets, signalling the industry’s growing commitment to lowering its emissions intensity.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

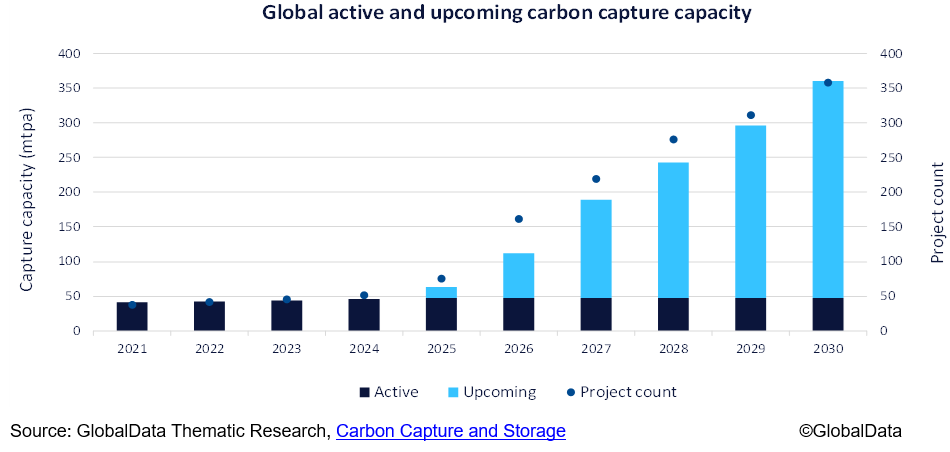

At the global level, more than 50 commercial-scale carbon capture projects were active within the energy sector alone as of 2024, representing a cumulative carbon capture capacity of 45 million tonnes per annum. There are 17 projects in advanced stages of development expected to begin operations in the second half of 2025 and 500 capture projects are under development globally across diverse industries, leading to significant capacity growth through 2030.

Despite advancements, several barriers hinder the scale-up of CCUS. The high cost of deployment — both capital investment and operational expenses — remains a key challenge. Infrastructure for CO₂ transport and storage is limited, and markets for utilising captured CO₂ are still emerging. Retrofitting existing industrial facilities adds another complexity, often making CCUS less less economically viable without strong policy support.

Regulatory uncertainty also limits investment confidence, with issues such as permitting delays, cross-border transport regulations and long-term liability for stored CO₂ needing clearer guidance. Public skepticism persists, with some stakeholders viewing CCUS as a way to prolong fossil fuel use rather than a climate mitigation tool. The lack of standardised technologies, monitoring frameworks and cohesive value chains also hampers efficient scale-up of CCUS.

Further discussion on the CCUS theme and its impact within energy sector, along with an overview of the competitive positions held by oil and gas companies, can be found in GlobalData’s new theme report, Carbon Capture and Storage.