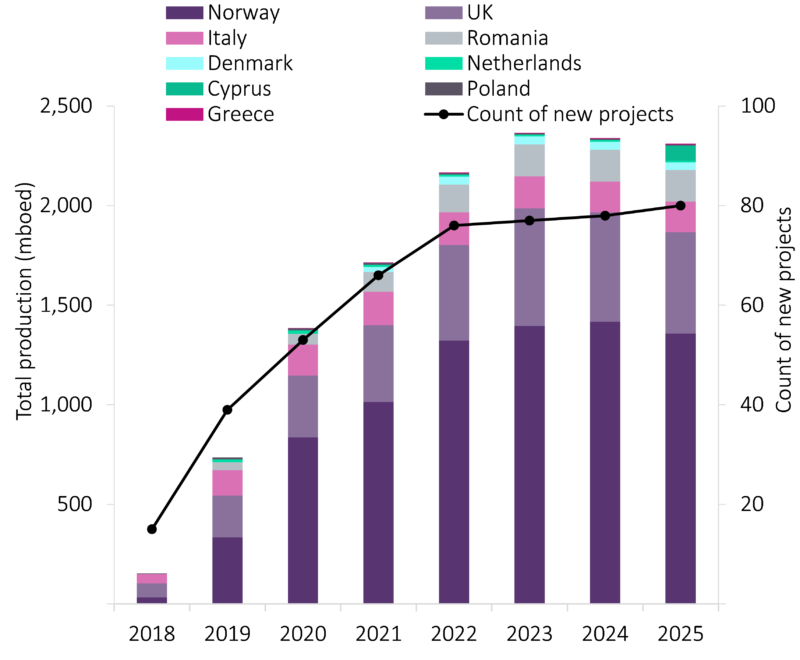

GlobalData expects that 81 new crude and natural gas projects will start operations in Europe over the next eight years. By 2025, the projects will contribute around 1,496 thousand barrels per day (mbd) to global oil production and close to 4.7 billion cubic feet per day (bcfd) to global gas production.

The majority of new developments, or 45 projects, fall under an early-stage category, while 36 of the new projects have progressed to well-defined development plans. Differentiating for the primary resource type, conventional oil and gas projects account for 38 new projects each. The region will see five heavy oil projects among its upcoming developments.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The UK will lead with a total of 37 projects, followed by Norway with 28 and Italy with six. Norway will drive natural gas production, contributing 1.6 bcfd to the region’s gas production by 2025. Norway will also be responsible for the largest contribution to oil and condensate production with the country’s upcoming projects, adding 1,072 mbd over the eight-year period.

Among companies participating in new projects in Europe, Statoil will see the highest contribution to its oil and condensate production from upcoming fields with 409.2 mbd by 2025. Upcoming projects in Europe will contribute 156.1 mbd to Petoro and 146.5 mbd to Lundin Petroleum by end of the eight-year period. On the gas side, Statoil will see 579 million cubic feet per day (mmcfd) brought in by new projects by 2025, followed by Po Valley Energy and OMV with 324 mmcfd and 323 mmcfd respectively.

Upcoming projects production in Europe, 2018 to 2025

Source: GlobalData Upstream Analytics

Offshore developments will be responsible for over 84% of Europe’s new gas production in 2025. Deepwater fields will bring 1,862 mmcfd, while shallow water and ultra-deepwater will contribute 1,668 and 452 mmcfd respectively. New onshore gas projects will add 764 mmcfd to the region’s gas production by 2025.

Similarly to gas, close to 97% of new oil production in 2025 will come from offshore fields. Shallow water fields will contribute 929 mbd, while deepwater and ultra-deepwater developments will bring on 515 and 1 mbd respectively by 2025. The remaining 3% of Europe’s oil and condensate production in 2025, or 51 mbd, will come from onshore fields.